share price has shown some weakness recently, but the financial outlook looks good: is the market wrong?")

It's hard to get excited about the Viking Mines (ASX:VKA) share price's recent performance, which has seen it drop 23% over the past month. However, if you look closely, you may notice that the key financial metrics look quite decent. This could mean the stock could rise over time, given how the market typically rewards more resilient long-term fundamentals. In particular, today we will pay attention to Viking Mines' ROE.

Return on equity or ROE is a key measure used to evaluate how efficiently a company's management is utilizing the company's capital. In other words, this reveals that the company has been successful in turning shareholder investments into profits.

Check out our latest analysis for Viking Mines.

How do I calculate return on equity?

of ROE calculation formula teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders' equity

So, based on the above formula, Viking Mines' ROE is:

13% = AUD 1.2 million ÷ AUD 9.5 million (based on the trailing twelve months to June 2023).

“Earnings” is the amount of your after-tax earnings over the past 12 months. So for every AU$1 of shareholders' equity, the company generated AU$0.13 of his profit.

What is the relationship between ROE and profit growth rate?

So far, we have learned that ROE is a measure of a company's profitability. Depending on how much of these profits a company reinvests or “retains”, and how effectively it does so, we are then able to assess a company's earnings growth potential. Assuming everything else remains constant, the higher the ROE and profit retention, the higher the company's growth rate compared to companies that don't necessarily have these characteristics.

Viking Mines' earnings growth and ROE of 13%

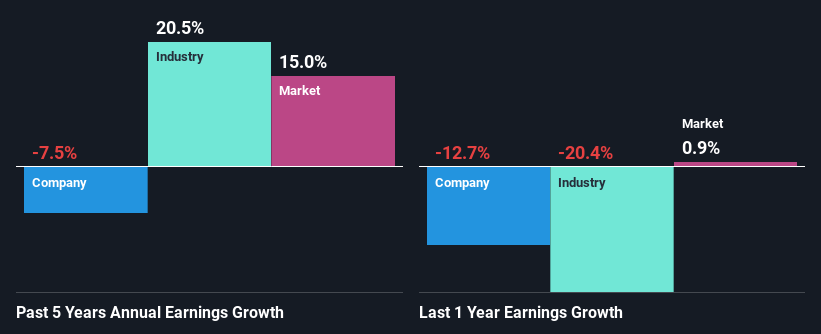

At first glance, Viking Mines appears to have a decent ROE. Moreover, his ROE for the company is very good compared to the industry average of 9.8%. Needless to say, we were quite surprised to see that Viking Mines' net income has declined at a rate of 7.5% over the past five years. We think there may be other factors at play here that are holding back the company's growth. These include low earnings retention and misallocation of capital.

However, when we compared Viking Mines's growth with its industry, we found that while the company's revenues have shrunk, the industry has seen its revenues grow at 21% over the same period. This is very worrying.

Earnings growth is an important metric to consider when evaluating a stock. It's important for investors to know whether the market is pricing in a company's expected earnings growth (or decline). That way, you'll know if the stock is headed for clear blue waters or if a swamp awaits. One good indicator of expected earnings growth is the P/E ratio, which determines the price the market is willing to pay for a stock based on its earnings outlook. So you might want to check whether Viking Mines is trading on a higher or lower P/E ratio, relative to its industry.

Is Viking Mine reinvesting its profits effectively?

Viking Mines does not pay dividends. That means all of the profits could potentially be reinvested back into the business, but if they keep all of the profits, that doesn't explain why the company's profits have declined. Therefore, there may be other explanations in this regard. For example, your company may be underperforming.

conclusion

Overall, there appear to be some positive aspects to Viking Mines' business. However, the low profit growth is a bit concerning, especially given that the company has a high rate of return and reinvests a large portion of its profits. There may be other factors inhibiting growth that are not necessarily in control of your business at first glance. We don't want to completely fire the company, but we do try to see how risky the business is in order to make more informed decisions about the company. The risks dashboard shows the four risks he has identified regarding Viking Mines.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.