With the news that inflation has increased Over the past month, many small and medium-sized businesses (SMBs) may have found themselves walking a tightrope with even fewer safety nets than usual. In the best cases, most small businesses have access to a variety of borrowing tools. However, rising inflation may reduce entrepreneurs' ability to borrow.

in “SMB Borrowing Trends: Trends, Tools, and Decision Factors” — with PYMNTS Intelligence us bank Report — We've identified several factors to help business owners decide which financing options make sense. The most important of these is annual income.

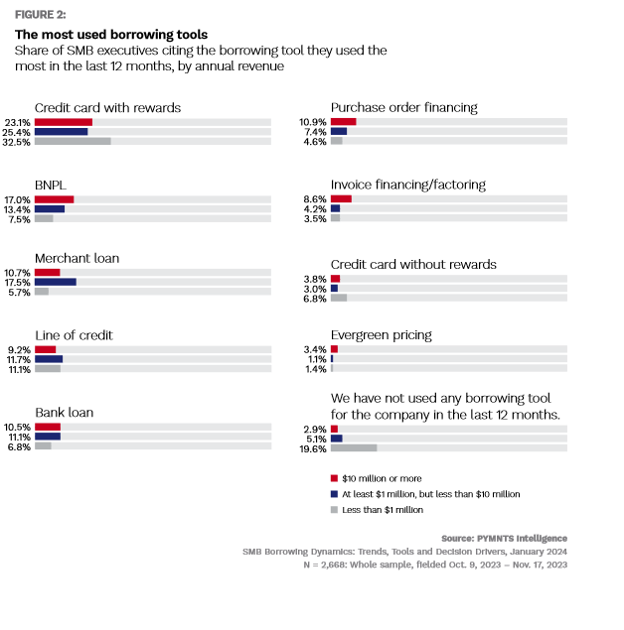

This report reflects feedback from 2,668 small business owners and found that low-profit small businesses prioritize immediate capital needs and financial stability over considerations of high-profit small businesses. It has become clear that there is a trend. This is in light of last year's volatile economic conditions, with nearly 20% of low-revenue small businesses (defined in the survey as those with less than $1 million in annual revenue) refusing to take advantage of any borrowing tools during that period. That might explain why.

But for nearly a third of low-profit small businesses, rewards credit cards were their funding source of choice last year. reason? The report found that rewards credit cards are attractive to this segment of small and medium-sized businesses because they offer “immediate benefits that deliver tangible value.”

In fact, rewards credit cards have been the most popular source of funding for all small businesses over the past 12 months. 23% of high-revenue small businesses (small businesses with annual revenue of $10 million to $25 million) used reward credit cards as a first-line defense borrowing tool. On the other hand, 17% of the high-profit segment utilized his BNPL financing option, while less than 8% of low-profit SMEs utilized this tool.

More than 25% of small businesses ($1 million to $10 million in revenue) in the center preferred rewards credit cards, and about 13% of them used BNPL funds to pay their bills.

While it remains to be seen how the latest inflation rates will affect small businesses, the dispersion in this data means that financial institutions (FIs) wishing to serve this market will have access to a variety of borrowing tools, especially those with special benefits. This suggests that we should focus on providing credit cards and credit cards. BNPL appeals to small and medium-sized businesses.

Financial institutions seeking to connect with small businesses with low profitability should be aware that this sector is particularly sensitive, but developing and marketing products that address the concerns of small businesses can help reduce their vigilance. Feelings can be overcome.