stock is strong, but fundamentals are unclear: What lies ahead?")

SAP (ETR:SAP) has been doing well on the stock market, with its share price increasing by a significant 18% over the past three months. However, the company's key financial metrics appear to be different across the board, which raises questions about whether the company's current share price momentum can be maintained. In particular, I would like to pay attention to SAP's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder as it indicates how effectively their capital is being reinvested. In other words, it is a profitability ratio that measures the rate of return on the capital provided by a company's shareholders.

Check out our latest analysis for SAP.

How do you calculate return on equity?

of Formula for calculating return on equity teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders' equity

So, based on the above formula, SAP's ROE is:

8.3% = €3.6 billion ÷ €43 billion (based on the trailing 12 months to December 2023).

“Return” is the annual profit. One way he conceptualizes this is that for every €1 of shareholders' equity, the company made his €0.08 in profit.

Why is ROE important for profit growth?

So far, we have learned that ROE measures how efficiently a company is generating its profits. We are then able to evaluate a company's future ability to generate profits based on how much of its profits it chooses to reinvest or “retain”. All else being equal, companies with higher return on equity and profit retention typically have higher growth rates compared to companies that don't have the same characteristics.

SAP's revenue growth and ROE of 8.3%

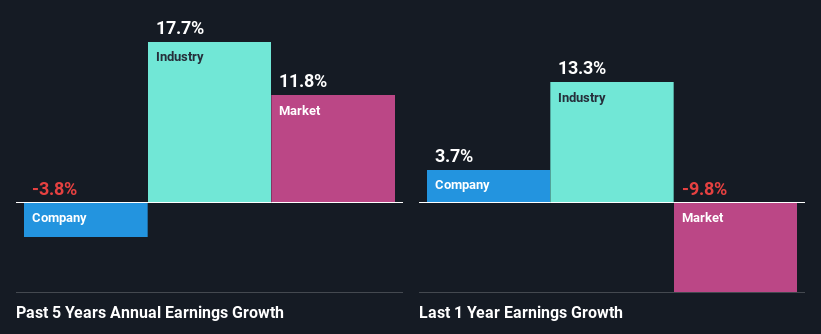

SAP's ROE doesn't look all that attractive at first glance. A quick look into it reveals that the company's ROE is below the industry average of 19%. Considering the circumstances, it's not surprising that SAP's net income has declined by 3.8% over the past five years. We believe there may be other aspects that are negatively impacting the company's earnings outlook. For example, a company may have poor capital allocation or a very high payout ratio.

However, when we compare SAP's growth with the industry, we find that the company's revenues have been shrinking, while the industry has seen its revenues grow at 18% over the same period. This is very worrying.

Earnings growth is an important metric to consider when evaluating a stock. It's important for investors to know whether the market is pricing in a company's expected earnings growth (or decline). Doing so will help you determine whether a stock's future is promising or ominous. Is the market pricing in SAP's future prospects? Find out in our latest Intrinsic Value infographic research report.

Is SAP leveraging its profits efficiently?

Despite having a typical three-year median payout ratio of 49% (retaining 51% of profits), SAP has experienced declining earnings as we saw above. Therefore, there may be other factors at play here that could potentially inhibit growth. For example, businesses are facing some headwinds.

Additionally, SAP has been paying a dividend for at least 10 years, suggesting that maintaining the dividend is far more important to management, even at the expense of business growth. According to existing analyst forecasts, the company's future dividend payout ratio is expected to drop to 36% in the next three years. As a result, the expected decline in SAP's dividend payout ratio explains that the company's future ROE is expected to rise to 17% over the same period.

conclusion

Overall, we have mixed feelings about SAP. Even if it appears to be retaining most of its profits, investors may not be benefiting from reinvestment after all, given the low ROE. Low revenue growth suggests that our theory is correct. Having said that, we researched the latest analyst forecasts and found that while the company has seen its earnings shrink in the past, analysts expect its future earnings to grow. To know more about the latest analyst forecasts for the company, check out this visualization of analyst forecasts for the company.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.