's annual report.")

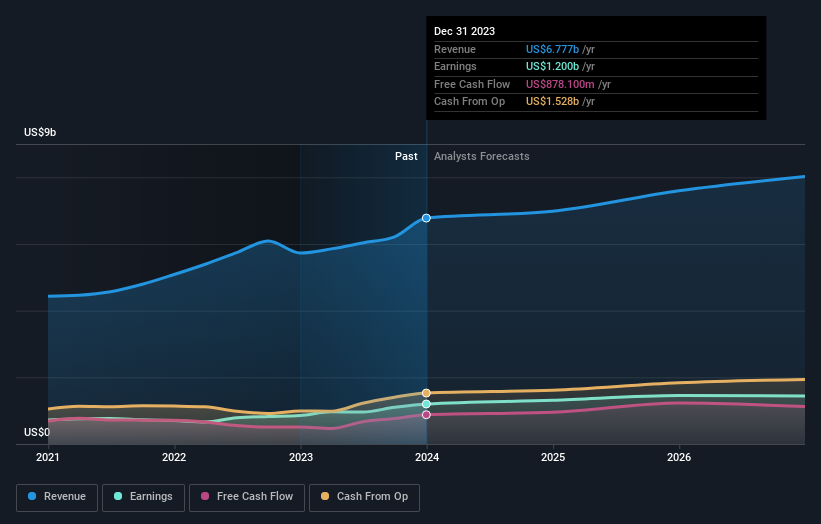

investors in Martin Marietta Materials, Inc. (NYSE:MLM) had a strong week, with its stock up 2.4% to close at $540 after reporting its full-year results. Martin Marietta Materials achieved revenue of US$6.8 billion and statutory earnings per share of US$18.82, in line with analyst forecasts, suggesting the business is on track to plan. reported. The analysts have updated their earnings model following these results, but it would be good to know whether they think there's been a big change to the company's outlook, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to find out what analysts are expecting for next year.

See the latest analysis for Martin Marietta Materials.

Following the latest results, Martin Marietta Materials' 16 analysts are now predicting revenue of US$6.98b in 2024. This is his 3.0% improvement in earnings compared to the previous 12 months, which is satisfactory. Earnings per share are expected to increase 8.8% to US$21.11. Prior to this earnings report, analysts had been forecasting 2024 revenue of US$7.31 billion and earnings per share (EPS) of US$20.90. The consensus is likely a bit more pessimistic, with earnings estimates revised downward following the latest earnings release. Change EPS forecast.

Despite the decline in earnings estimates, the average target price remained steady at US$560. This probably suggests that analysts are more focused on earnings. It may also be useful to examine the range of analysts' estimates to assess how different the outlier's opinion is from the average. Currently, the most bullish analyst values Martin Marietta Materials at $642 per share, while the most bearish values it at $350. There are certainly some differing views on the stock price, but in our view the range of estimates is not wide enough to suggest that the situation is unpredictable.

One way to get more context about these forecasts is to compare them to their past performance and to the performance of other companies in the same industry. We would like to emphasize that Martin Marietta Materials' revenue growth is expected to slow, with the expected annual growth rate of 3.0% to the end of 2024 being significantly lower than the historical annual growth rate of 10% over the past five years. I think. Compare this to other companies in the industry, which are expected to see combined annual revenue growth of 6.3% (analyst estimates). Considering the expected slowdown in growth, it's clear that Martin Marietta Materials is also expected to grow more slowly than other industry participants.

conclusion

Most importantly, there was no major change in sentiment, with the analysts reaffirming that the business is performing in line with previous earnings per share estimates. On the downside, the company has also lowered its earnings forecast, with some forecasts suggesting it will do worse than the industry as a whole. Still, he cares more about earnings per share for the intrinsic value of the business. There was no actual change to the consensus target price, suggesting that the intrinsic value of the business has not changed significantly at the latest estimate.

With that in mind, we can't jump to any conclusions about Martin Marietta Materials. Long-term profitability is far more important than next year's profits. His forecast for Martin Marietta Materials to 2026 is available for free on this platform.

It may also be worth using the debt analysis tool on the Simply Wall St platform to consider whether Martin Marietta Materials's debt burden is appropriate.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.