stock's strong financial outlook the driving force behind its momentum?")

Most readers would already know that the Netcall (LON:NET) share price has increased by a significant 6.7% in the last month. Since the market usually pays for a company's long-term fundamentals, we decided to investigate whether a company's key performance indicators are influencing the market. In particular, today I would like to pay attention to Netcall's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder as it indicates how effectively their capital is being reinvested. More simply, it measures a company's profitability in relation to shareholder equity.

See our latest analysis for Netcall

How is ROE calculated?

of ROE calculation formula teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders' equity

So, based on the above formula, Netcall's ROE is:

14% = GBP 5.4 million ÷ GBP 38 million (based on the trailing twelve months to December 2023).

“Earnings” is the amount of your after-tax earnings over the past 12 months. This means that for every £1 a shareholder invests, the company generates £0.14 in profit for him.

What is the relationship between ROE and profit growth rate?

So far, we have learned that ROE is a measure of a company's profitability. Now we need to assess how much profit the company reinvests or “retains” for future growth, which gives us an idea about the company's growth potential. Assuming everything else remains constant, the higher the ROE and profit retention, the higher the company's growth rate compared to companies that don't necessarily have these characteristics.

Netcall's revenue growth and 14% ROE

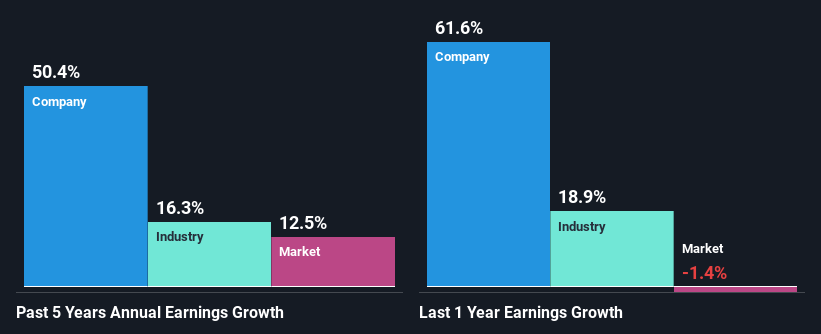

First, Netcall appears to have a respectable ROE. His ROE for the company looks pretty good, especially when compared to the industry average of 9.1%. This certainly lends some context to the exceptional 50% growth in Netcall's net income over the past five years. However, there may be other causes behind this growth. For example, the company's management may have made some good strategic decisions, or the company may have a low dividend payout ratio.

Next, if we compare it to the industry's net income growth rate, we find that Netcall's growth rate is very high compared to the industry average growth rate of 16% over the same period, which is great.

Earnings growth is a big factor in stock valuation. It's important for investors to know whether the market is pricing in a company's expected earnings growth (or decline). That way, you'll know if the stock is headed for clear blue waters or if a swamp awaits. One good indicator of expected earnings growth is his P/E ratio, which determines the price the market is willing to pay for a stock based on its earnings outlook. So you might want to check whether Netcall is trading on a higher or lower P/E relative to its industry.

Is Netcall effectively utilizing its retained earnings?

Netcall's median three-year payout ratio is 28%, which is a bit low. The company will hold the remaining 72%. Therefore, Netcall appears to have delivered impressive growth in earnings (discussed above) and reinvested them efficiently in a way that pays well-covered dividends.

Additionally, Netcall has been paying dividends for at least 10 years. This shows that the company is committed to sharing profits with shareholders.

summary

Overall, I'm very happy with Netcall's performance. In particular, it's great to see that the company has invested heavily in its business, delivering strong revenue growth along with high rates of return. If the company continues to grow its revenue as it has been, it could have a positive impact on the stock price, given how earnings per share affect the stock price over the long term. Remember, the stock price outcome also depends on the underlying risks that the company may face. Therefore, it is important for investors to be aware of the risks associated with the business. The risks dashboard shows the two risks he has identified regarding Netcall.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.