pays a dividend of CAD 0.0575")

board of directors of Timbercreek Financial Corporation (TSE:TF) has announced that it will pay a dividend on February 15th, with investors receiving C$0.0575 per share. The dividend yield based on this payment is 9.5%, which is still above the industry average.

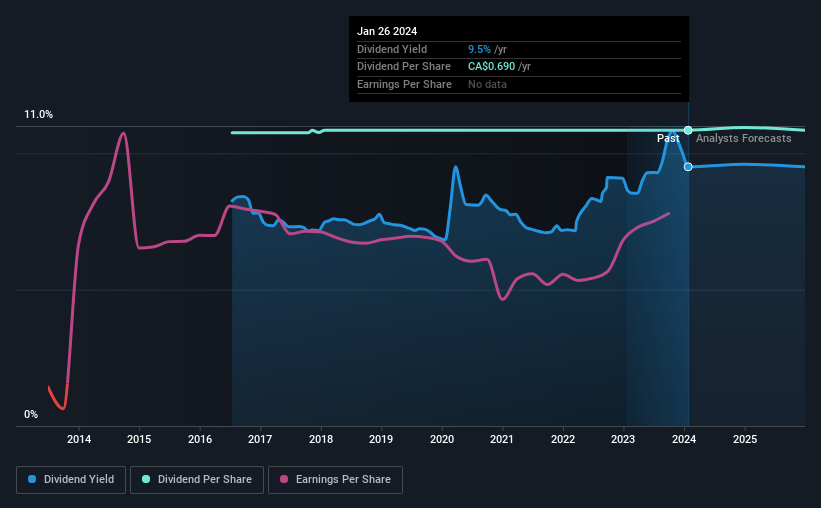

Check out our latest analysis for Timbercreek Financial.

Timbercreek Financial pays out more than it earns.

It's great to have a high dividend yield, but you also need to consider whether the payments are sustainable. Prior to this announcement, Timbercreek Financial's dividends accounted for a sizable portion of its profit, but only 60% of its free cash flow. Since dividends only pay out cash to shareholders, we focus on the cash payout ratio, which shows that there is enough money left over to reinvest in the business.

Looking ahead, earnings per share are expected to decline by 11.8% over the next year. If the dividend continues on its recent trajectory, the payout ratio after 12 months could be 101%, which is definitely a bit high to be sustainable going forward.

Timbercreek Financial continues to build on its track record

This dividend track record is pretty solid, but since it's only been around for 8 years, we'd like to see a few more years of history before drawing any firm conclusions. Since 2016, his annual payment at that time was CAD 0.684. In contrast, the most recent annual payment was CAD 0.69. Dividends grew less than 1% per year during this period. It's good to see at least some dividend growth. However, given the relatively short history of dividend payments, we don't want to rely too much on this dividend.

Dividend increases may be difficult to achieve

Some investors may be chomping at the bit to buy the company's stock based on its dividend history. Over the past five years, earnings have grown at 4.1% per year, which admittedly is a bit slow. Revenues haven't been growing quickly at all, and the company is paying out most of its profits as dividends. If a company prefers to pay cash to shareholders rather than reinvest it, this can often say a lot about its dividend prospects.

In summary

Overall, I don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. The payouts aren't particularly stable, and we don't see much growth potential, but the dividend is well covered by cash flow, so it could prove reliable in the short term. You'll probably look elsewhere for more profitable investments.

Investors generally prefer companies with consistent and stable dividend policies over companies with irregular dividend policies. However, there are other things investors should consider when analyzing stock performance. As just one example, we found that 3 warning signs for Timbercreek Financial Two of them are concerning.Looking for more high-yield dividend ideas? Try ours A group of people with strong dividends.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodologies, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.